Rachel Kurzius

Rachel Kurzius

Demonstrators call for fossil fuel divestment in Dupont Circle in February 2015. (Photo via 350.org)

Demonstrators call for fossil fuel divestment in Dupont Circle in February 2015. (Photo via 350.org)

Following a three-year campaign, DC Divest is claiming victory—the D.C. government has sold off its pension fund’s direct investments in coal, oil, and gas companies.

This morning, the group announced that the D.C. Retirement Board has officially sold off around $6.5 million in direct investments in the 200 companies with the most fossil fuel reserves. In 2013, that amounted to around 0.1 percent of the total fund, which is now around $6.4 billion. D.C. is the second-largest city in the country to divest, after San Francisco.

“We’ve gone from being a fringe thing to seeing the Rockefellers divest,” says Hayden Higgins, a member of DC Divest. “When we started, this wasn’t something people really knew about but something happened that was totally historic because a couple dozen people decided to meet every Tuesday for three years.”

Around the same time that DC Divest was forming in 2013, the DCRB adopted a policy statement about considering whether the fund could help achieve environment, social, and governance goals in its decision-making, so long as “they are consistent with our obligations to the participants and beneficiaries of the District of Columbia Teachers’ Retirement Plan and the District of Columbia Firefighters and Police Officers’ Retirement Plan and with the standard of care established by the prudent investor rule.”

The D.C. Council passed a resolution for the DCRB to “explore all means possible for minimizing the District’s involvement with companies with the largest fossil fuel reserves” in December of 2014. More binding legislation was introduced in both 2013 and 2015, but never reached a vote.

The notion of judging companies based on their fossil fuel reserves comes from environmentalist Bill McKibben’s theory that 80 percent of coal, gas, and oil reserves that are currently owned by companies needs to stay in the ground to avoid further environmental catastrophe.

D.C. faces the threat of significant flooding from the rise of ocean waters. More than 19 environmental and citizen groups supported the fossil fuel divestment, including the Sierra Club, Hip Hop Caucus, and the Chesapeake Climate Action Network.

“The Retirement Board looks at numbers … Part of what [DC Divest] did was help make the financial case—this is a bad investment. It is going down. So not only is this the right thing to do for our future, for our sustainability, but this the right thing to do just on pure economics,” said Ward 6 Councilmember Charles Allen at the announcement this morning.

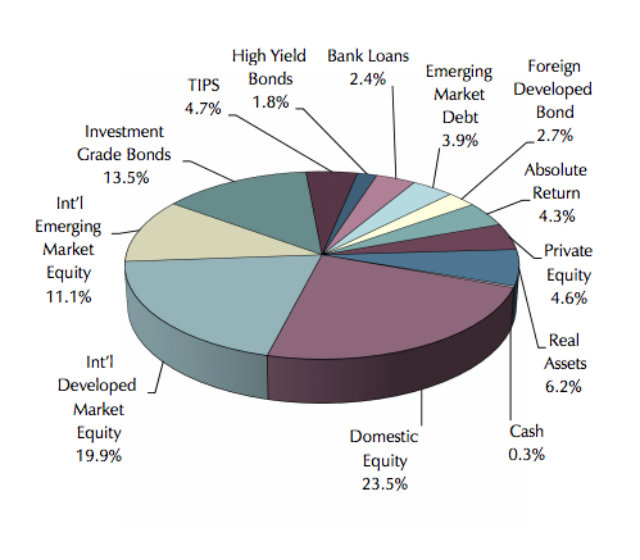

The most recent quarterly report on March 31 of this year shows the pension fund’s assets distributed like this:

Image via D.C. Retirement Board.

Image via D.C. Retirement Board.

Divestment involves getting rid of direct investments, but co-mingled funds, like hedge or mutual funds, might still include fossil fuel company investments. Looking into that is “definitely a goal of ours down the road as best practices emerge,” says Higgins of DC Divest.

Tomorrow the D.C. Council will vote on a ceremonial resolution in favor of DCRB’s decision, which Allen, Chairman Phil Mendelson, At-large Councilmember David Grosso and Ward 3 Councilmember Mary Cheh will co-introduce.

Not everyone is pleased with the announcement. “This is an empty gesture, pure and simple,” says Matt Dempsey, spokesperson for the Independent Petroleum Association of America.

This isn’t the first divestment for DCRB—the fund is prohibited from investment in certain companies that do business with the governments of Iran and Sudan, and previously banned business with the South African apartheid government. Georgetown University’s board of directors voted last June to divest its endowment from companies that mine coal.

Updated with comment from Matt Dempsey.