Photo by Michael Galkovsky.

Photo by Michael Galkovsky.

By WAMU’s Meg Anderson

D.C. residents are some of the most burdened by student debt in the country. Now, a new bill seeks to lighten some of that load.

The legislation, called the Student Loan Authority Establishment Act and introduced on Tuesday by At-Large Councilmember Elissa Silverman, would create an independent agency that would issue and refinance student loans for the city’s residents and students at D.C. colleges and universities. Silverman says she expects a hearing on the bill early next year.

“Our residents are overwhelmed with debt, particularly student loan debt,” Silverman says. “I think what we’re trying to do is enhance our tools to make the District more affordable and more equitable.”

If passed, the student loan authority would be funded through the use of tax-exempt bonds, and would issue loans at a lower interest rate than federal loans, which range from about 5 to 7 percent, or private loans, which are set by private lenders and can run as high as 14 percent. According to Silverman, the agency would be similar to the D.C. Housing Finance Agency, which uses tax-exempt bonds to lower developers’ costs in building rental housing and reduces the costs for homeowners by offering mortgage rates below the market rate and assisting with down payments. Silverman says beyond initial seed money to get the new agency off the ground, she expects it to be self-sustaining.

The specific interest rates for the proposed program have not been determined yet, but a spokesperson for Silverman says the D.C. agency would not have the overhead costs of both federal and private loans, which contribute to higher interest rates.

The loans offered and refinanced through the agency, which would include undergraduate, graduate, and parent loans, would be eligible for income-based repayment plans and public service loan forgiveness, in which student debt is forgiven after working in the public sector, including nonprofits, for a certain period.

More than a dozen states already have similar agencies that offer loans for students attending colleges in the state or for residents of the state, including Massachusetts, South Carolina, and New Jersey.

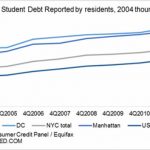

Debt from student loans is a growing problem across the country. Students nationwide owe about $1.5 trillion in student loans. In 2017, more than half of 18 to 29-year-olds who received an undergraduate degree took on student debt, and one in five people who have student debt are behind on their payments. In D.C., the average debt for the class of 2017 was more than $30,000.

The effect of student loan debt can be far-reaching and lasting: It can delay buying a home by as much as seven years, according to a 2017 survey, and it can prevent people from saving for retirement or emergencies.

“The burden of debt prevents our residents from buying a home or having a family because they just don’t want to do it when they have so much student loan debt,” says Silverman. “That has real impact on people’s lives and on the district itself.”

Silverman says she has been paying her own student loans off for about 20 years now. She has about $500 left.

This story was originally published on WAMU.